10-K: Annual report pursuant to Section 13 and 15(d)

Published on

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM

For the fiscal year ended

For the transition period from to

Commission file number

(Exact name of registrant as specified in its charter)

(State or other jurisdiction of |

(I.R.S. Employer |

|

incorporation or organization) |

Identification No.) |

|

(Address of principal executive offices) |

(State) |

(Zip Code) |

( |

(Registrant’s telephone number, including area code) |

Securities registered pursuant to 12(b) of the Exchange Act:

Title of each class |

Trading Symbol |

Name of each exchange on which registered |

The |

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ☐

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or 15(d) of the Act. Yes ☐

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days.

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files).

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

Large accelerated filer ☐ |

Accelerated filer ☐ |

Smaller reporting company |

Emerging growth company |

If an emerging growth company, indicate by checkmark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the registrant has filed a report on and attestation to its management’s assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting firm that prepared or issued its audit report.

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes

If securities are registered pursuant to Section 12(b) of the Act, indicate by check mark whether the financial statements of the registrant included in the filing reflect the correction of an error to previously issued financial statements. ☐

Indicate by check mark whether any of those error corrections are restatements that are required a recovery analysis of incentive-based compensation received by any of the registrant’s executive officers during the relevant recovery period pursuant to 240.10D-1(b). ☐

The aggregate market value of voting common stock held by non-affiliates of the registrant as of June 30, 2022, the last business day of the registrant’s second fiscal quarter, was approximately $

There were

DOCUMENTS INCORPORATED BY REFERENCE

Certain information required for Items 10, 11, 12, 13 and 14 of Part III of this Annual Report on Form 10-K is incorporated by reference to the registrant’s definitive proxy statement for the 2023 annual meeting of stockholders.

TERAWULF INC.

TABLE OF CONTENTS

(i)

EXPLANATORY NOTE

Restatement of Previously Issued Financial Statements

As part of the Company’s financial statement close process and preparation of its Annual Report on Form 10-K (the “2022 Form 10-K”), the Company identified errors in its historical interim unaudited consolidated financial statements. The misstatements relate solely to incorrectly calculating the impact of noncash activity on purchase and deposits on plant and equipment, resulting in an understatement of net cash used in investing activities and a corresponding overstatement of net cash used in operating activities as originally included in the respective interim unaudited consolidated statements of cash flows. The Company determined that its interim unaudited consolidated financial statements for the quarterly periods ended March 31, 2022, June 30, 2022 and September 30, 2022 (the “Relevant Periods”) were materially misstated and needed to be restated. The restatements are set forth in detail in Note 18 to the Consolidated Financial Statements.

Internal Control & Disclosure Control Considerations

Management assessed the effectiveness of internal control over financial reporting and identified a material weakness, resulting in the conclusion by our Chief Executive Officer and Chief Financial Officer that our internal control over financial reporting and our disclosure controls and procedures were not effective as of December 31, 2022. The material weakness solely relates to the inadequate design and operation of management’s review controls over calculating the impact of noncash activity on purchase and deposits on plant and equipment in the consolidated statement of cash flows. Management is taking steps to remediate the material weakness in our internal control over financial reporting, as described in Part II, Item 9A, “Controls and Procedures.”

Non-Reliance on Previously Filed Reports

TeraWulf believes that presenting all of this information regarding the Relevant Periods in this 2022 Form 10-K allows investors to review all pertinent data in a single presentation. Therefore, we do not plan to amend our previously filed Quarterly Reports on Form 10-Q for the Relevant Periods. Accordingly, investors should no longer rely upon the Company’s previously released financial statements for the Relevant Periods and any earnings releases or other communications relating to these Relevant Periods. The financial information that has been previously filed or otherwise reported for the Relevant Periods is superseded by the information in this 2022 Form 10-K. TeraWulf will also correct previously reported financial information for this error in its future filings, as applicable.

For discussions of the restatement adjustments, see Item 1A, “Risk Factors” and Item 8, “Financial Statements,” including Notes 2 and 18 of the Notes to the Consolidated Financial Statements.

(i)

PART I

ITEM 1. |

Business |

Overview

TeraWulf, Inc. (“TeraWulf”, the “Company”, “our” or “we”) is a digital asset technology company with a core business of digital infrastructure and energy development to enable sustainable bitcoin mining. TeraWulf develops, owns and operates its bitcoin mining facility sites in the United States using nuclear, hydro and solar energy sources, currently consuming over 91% zero-carbon energy, with a target of 100% zero-carbon energy by 2028. TeraWulf began trading on Nasdaq under the symbol “WULF” on December 14, 2021, following its successful strategic business combination with RM 101 Inc. (formerly known as IKONICS Corporation).

TeraWulf commenced industrial scale bitcoin mining in March 2022 and is currently operating two near zero-carbon data centers in New York and Pennsylvania, the Lake Mariner Facility and the Nautilus Cryptomine Facility, respectively. TeraWulf began mining bitcoin at the Lake Mariner Facility in March 2022 and at the Nautilus Cryptomine Facility in February 2023. As of March 30, 2023, these two industrial-scale projects had a self-mining hash rate of 2.8 exahash per second (“EH/s”) with approximately 28,000 miners currently deployed, comprised of 18,000 operational miners at the Lake Mariner Facility (13,000 self-miners and 5,000 hosted miners) and 10,000 self-miners at the Nautilus Cryptomine Facility. TeraWulf’s facilities are expected to reach an aggregate 160 MW of net bitcoin mining capacity with a capacity to support 50,000 miners and over 5.5 EH/s of computational power in the second quarter of 2023.

Our primary source of revenue is from sustainably mining bitcoin at our bitcoin mining facility sites. We also earn revenue from miner hosting services to third parties. We do not hold, sell or transact in bitcoin or any other digital assets for anyone other than ourselves. We do not hedge our bitcoin.

Our industrial scale bitcoin mining operations focus on maximizing our ability to successfully mine bitcoin by growing our hash rate (the amount of computer power we devote to supporting the bitcoin blockchain) to increase our chances of successfully finding cryptographic hashes that create new blocks on the bitcoin blockchain (a process known as “solving a block”). Generally, the greater share of the bitcoin blockchain’s total network hash rate (the aggregate hash rate deployed to solving a block on the bitcoin blockchain) represented by a miner’s hash rate, the greater the miner’s chances of solving a block and therefore earning the block reward, which is currently 6.25 bitcoin plus transaction fees per block. As additional miner operators enter the market in response to increased demand for bitcoin, the bitcoin blockchain’s network hash rate grows.

The majority of our revenue comes from our self-mined bitcoin, which we store and safeguard in a cold storage wallet held by our custodian, NYDIG Trust Company LLC (“NYDIG”), a duly chartered New York limited liability trust company. We participate in a mining pool operated by Foundry Digital LLC (“Foundry”), and at the end of each day, our earned bitcoin is sent by Foundry to our wallet address custodied with NYDIG. Any bitcoin mined by third-party miners hosted at our Lake Mariner Data LLC (“Lake Mariner”) facility site is either (1) delivered directly into the third-party miners’ wallets, which we have neither access to nor oversight over, or (2) delivered into our wallet held by NYDIG, pursuant to the mined bitcoin sharing arrangements agreed to in our respective miner hosting agreements. To the extent we sell any of our mined bitcoin, we do so using NYDIG Execution LLC (“NYDIG Execution”), a Delaware LLC registered as a Money Services Business with the Financial Crimes Enforcement Network and licensed with a BitLicense by the New York State Department of Financial Services. Funds from the sale of our bitcoin by NYDIG Execution are deposited by NYDIG Execution directly into the Company’s bank account at a U.S. depository institution. We do not currently sell or intend to sell our bitcoin on any exchange. Instead, we rely on NYDIG Execution to sell any of our mined bitcoin, pursuant to our execution agreement with NYDIG which is described further in the section titled “Risk Factors” herein. We sell bitcoin on a daily, weekly and monthly basis to pay for all operating expenses of the Company.

As described further in the section titled “Risk Factors” herein, even though we do not hold any cryptocurrency on others’ behalf and do not currently sell or intend to sell our cryptocurrency on exchanges, our business, financial condition and results of operations may still be adversely affected by recent industry-wide developments beyond our control, including the continued industry-wide fallout from (i) the recent ceasing of operations by Silicon Valley Bank, Signature Bank (“SBNY”) and Silvergate Bank and (ii) the recent Chapter 11 bankruptcy filings of cryptocurrency exchange FTX Trading Ltd., et al. (“FTX”) (including its affiliated hedge fund Alameda Research LLC), crypto hedge fund Three Arrows Capital (“Three Arrows”) and crypto lenders Celsius Network LLC, et al. (“Celsius”), Voyager Digital Ltd., et al. (“Voyager”), BlockFi Inc., et al. (“BlockFi”) and Genesis Global Holdco, LLC, et al. (“Genesis”). While we have no exposure to FTX, Three Arrows, Celsius, Voyager or BlockFi, Genesis is owned by Digital Currency

1

Group Inc. (“DCG”), who also owns Foundry, our mining pool provider. At this time, there are no material risks to our business arising from our indirect exposure to Genesis. Most recently, in March 2023, SVB Financial, the parent of Silicon Valley Bank, filed for Chapter 11 bankruptcy.

We have no material direct exposure to SVB Financial, Silicon Valley Bank or Silvergate Bank. Although (i) our cryptocurrency mining business has (x) no direct exposure to any of the cryptocurrency market participants that recently filed for Chapter 11 bankruptcy and (y) no material direct exposure to SVB Financial, Silicon Valley Bank or Silvergate Bank; (ii) we have no assets, material or otherwise, that may not be recovered due to the foregoing bankruptcies or bank shutdowns; (iii) we have no direct exposure to any other counterparties, customers, custodians or other financial institutions or crypto asset market participants known to have (x) experienced excessive redemptions or suspended redemptions or withdrawal of crypto assets, (y) the crypto assets of their customers unaccounted for, or (z) experienced material corporate compliance failures; and (iv) our activities in the commercial optimization of the power supply are unaffected by the recent crypto market and banking industry events; our business, financial condition and results of operations may not be immune to unfavorable investor sentiment resulting from these recent developments in the broader cryptocurrency and banking industries.

On March 12, 2023, Signature Bank (“SBNY”) was closed by its state chartering authority, the New York State Department of Financial Services. On the same date the Federal Deposit Insurance Corporation (“FDIC”) was appointed as receiver and transferred all customer deposits and substantially all of the assets of SBNY to Signature Bridge Bank, N.A., a full-service bank that is being operated by the FDIC. The FDIC, the U.S. Treasury, and the Federal Reserve jointly announced that all depositors of SBNY would be made whole, regardless of deposit insurance limits. The Company automatically became a customer of Signature Bridge Bank, N.A. as part of this action. Normal banking activities resumed on Monday, March 13, 2023. On March 29, 2023, the Company was advised by the FDIC that the Company’s bank accounts would be closed on April 5, 2023 and any remaining funds as of that date would be distributed to the Company by check. As of March 30, 2023, the Company held approximately $0.9 million in the former SBNY accounts and intends to transfer all then remaining funds out of Signature Bridge Bank, N.A. by April 5, 2023.

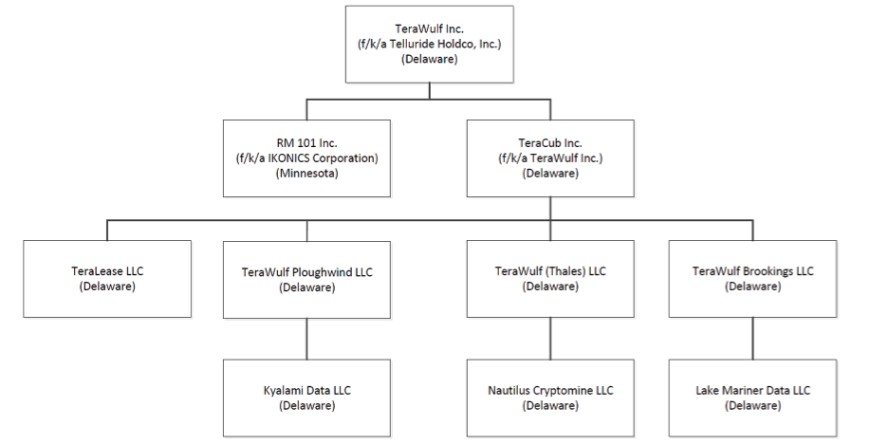

Corporate History and Structure

Paul Prager, Chief Executive Officer (“CEO”) and chairman of the board of directors of TeraWulf, co-founded TeraWulf with Nazar Khan, Chief Operating Officer and Chief Technology Officer, in 2021. Together with Kerri Langlais, Chief Strategy Officer, the TeraWulf management team has worked together for over 15 years.

TeraWulf’s business operations are conducted through several operating subsidiaries with its core operational and business activities directed through TeraWulf. The chart below sets forth TeraWulf’s corporate structure as of the date of this Annual Report. All entities on the chart have been incorporated in the State of Delaware or Minnesota as either corporations or limited liability companies, as the case may be, as indicated on the chart:

2

RM 101 Inc. (formerly known as IKONICS Corporation)

TeraWulf completed its business combination with RM 101 Inc. (formerly known as IKONICS Corporation) on December 13, 2021 (the “Closing Date”) pursuant to the agreement and plan of merger, dated as of June 24, 2021 (as amended, the “Merger Agreement”). Under the terms of the Merger Agreement, each share of RM 101 Inc. (formerly known as IKONICS Corporation) common stock issued and outstanding immediately prior to the Closing Date was automatically converted into and exchanged for (i) one validly issued, fully paid and nonassessable share of common stock of TeraWulf, (ii) one contractual contingent value right (each, a “CVR”) pursuant to the Contingent Value Rights Agreement between TeraWulf and RM 101 Inc. (formerly known as IKONICS Corporation) (the “CVR Agreement”) and (iii) the right to receive $5.00 in cash, without interest.

The TeraWulf Advantage: Vertically integrated, Zero-Carbon Bitcoin Miner

Vertical Integration. TeraWulf owns 100% of the Lake Mariner Facility and 25% of the Nautilus Cryptomine Facility. TeraWulf believes its ownership of its bitcoin mining facility sites is vital to its success, as it maximizes efficiency and reduces production cost. Energy infrastructure assets are complex and require specialized equipment, numerous commercial relationships, and diverse stakeholder groups. Ownership of its mining sites allows TeraWulf to take a wholistic approach to ensure projects are completed safely, timely, and reliably. In addition, vertical integration allows TeraWulf to be good stewards of the environment and the communities in which it operates. Furthermore, ownership enhances the ability to actively manage site development, the project supply chain, and commercial arrangements. Most importantly, it provides employees, investors, and communities accountability and transparency.

Environmentally Clean. TeraWulf’s strategy is to be the market leader for sustainable bitcoin mining. TeraWulf’s two bitcoin mining facilities are currently powered by more than 91% zero-carbon energy with a goal of utilizing 100% zero-carbon energy. The Nautilus Cryptomine Facility is powered by 100% zero-carbon nuclear energy and the Lake Mariner Facility in New York sources power in Western New York where over 91% of market energy comes from zero-carbon resources, primarily hydro and nuclear. Given the power-intensive nature of bitcoin mining and the implications for the environment, TeraWulf believes that its access to inexpensive, zero-carbon power represents a meaningful and durable competitive advantage for the Company relative to its publicly traded bitcoin mining peers.

Low Cost Energy Supply. TeraWulf expects to have one of the lowest electricity costs among its publicly traded bitcoin mining peers at approximately $0.035 per kilowatt-hour, augmenting TeraWulf’s competitive position in varying bitcoin price environments. The Nautilus Cryptomine Facility benefits from a contracted, fixed price of power of $0.02 per kilowatt-hour for a term of five years. TeraWulf anticipates the market cost of power at the Lake Mariner Facility will average approximately $0.045 per kilowatt-hour. TeraWulf’s Lake Mariner Facility and the Nautilus Cryptomine Facility are located at structurally congested points in their respective markets and may increase power optimization opportunities and the ability to provide ancillary services to the electrical distribution grid.

Scale Rapidly with Proprietary Expansion Pipeline. TeraWulf’s ability to achieve scale in its mining operations is driven by its access to state-of-the-art miners, ability to structure competitive power supply arrangements, and deep energy infrastructure and operational expertise. TeraWulf has the ability to significantly expand mining operations at its existing site. The Lake Mariner Facility has the ability to expand another 80 MW in the near term, and up to 500 MW in total. TeraWulf also retains the option to expand its mining capacity at the Nautilus Cryptomine Facility by 50 MW. In addition to its proprietary expansion capacity, TeraWulf has developed a strong, collaborative relationship with the leading mining equipment manufacturer, Bitmain. This strategic relationship supports preferred access and advantaged cost structures for Bitmain’s ASIC miners.

Experienced Team. TeraWulf is supported by Beowulf Electricity & Data Inc. (“Beowulf E&D”), a company controlled by TeraWulf’s CEO, to ensure an efficient buildout of its bitcoin mining facility sites. In addition, members of the Beowulf E&D team have over thirty years of experience overseeing the buildout and operation of large-scale energy facilities, which experience lends itself to the buildout of TeraWulf’s new bitcoin mining facilities. The Lake Mariner Facility is designed as replicable, reliable and cost-effective data centers for housing ASICs, but also designed with modular functionality to allow installation of a portion of ASICs prior to the completion of the facility.

Human Capital Management

As of March 30, 2023, TeraWulf had eight full-time employees. TeraWulf’s human capital resource objectives include identifying, recruiting, retaining, incentivizing and integrating TeraWulf’s employees, advisors and consultants. TeraWulf provides

3

employees the opportunity to advance professionally and to be rewarded commensurate with results. As TeraWulf is a small team of only eight employees, TeraWulf also uses its affiliate Beowulf E&D’s human capital resources for support pursuant to the administrative and infrastructure services agreement. Beowulf E&D, along with TeraWulf, is focused on ESG and diversity initiatives, and both companies share similar goals, corporate standards and governance practices as a result of their affiliated relationship. The principal purpose of TeraWulf’s 2021 Omnibus Incentive Plan is to attract, retain and motivate employees, executive officers and directors through the granting of stock-based compensation awards.

Planned Mining Operations

TeraWulf commenced industrial scale bitcoin mining in March 2022 and is currently operating two near zero-carbon data centers in New York and Pennsylvania. TeraWulf began mining bitcoin at the Lake Mariner Facility in March 2022 and at the Nautilus Cryptomine Facility in February 2023. As of March 30, 2023, these two industrial-scale projects had a self-mining hash rate of 2.8 EH/s with approximately 28,000 miners currently deployed, comprised of 18,000 operational miners at the Lake Mariner Facility (13,000 self-miners and 5,000 hosted miners) and 10,000 self-miners at the Nautilus Cryptomine Facility. TeraWulf’s facilities are expected to reach an aggregate 160 MW of net bitcoin mining capacity with a capacity to support 50,000 miners and over 5.5 EH/s of computational power in the second quarter of 2023.

Lake Mariner Facility — Located at a site adjacent to the decommissioned coal-fired Somerset Generating Station in Barker, New York, the Lake Mariner Facility has secured an initial 90 MW of energy to support its bitcoin mining capacity through an agreement with the New York Power Authority (“NYPA”) with the potential to expand into an additional 410 MW of energy supply. The Lake Mariner Facility began mining operations in March 2022 and as of March 30, 2023, has approximately 60 MW of operational mining capacity, representing approximately 18,000 miners. TeraWulf expects to reach 110 MW of mining capacity at the facility, representing approximately 34,000 miners, in the second quarter of 2023 pending the completion of construction of Building 2, which will add another 50 MW of mining capacity. The Lake Mariner Facility has the ability to expand another 80 MW in the near term, and up to 500 MW in total.

Nautilus Cryptomine Facility — Co-located with the 2.5 GW nuclear-powered Susquehanna Steam Electric Station in Berwick, Pennsylvania (the “Susquehanna Station”), 2.3 GW of which are owned and operated by Talen Energy Corporation (“Talen”), the Nautilus Cryptomine Facility nuclear-powered bitcoin mining facility with a current capacity of 200 MW. The Nautilus Cryptomine is a joint venture between TeraWulf and Cumulus Coin, LLC, a subsidiary of Talen. TeraWulf owns a 25% equity interest in the facility, which represents 50 MW of mining capacity. The Nautilus Cryptomine Facility is not connected to the electrical distribution grid, but is rather “behind-the-meter”, thereby avoiding transmission and distribution charges typically paid by other large power consumers. The Nautilus Cryptomine Facility receives nuclear power directly from a substation connected to the Susquehanna Station’s electrical generators, which is contractually priced at a fixed cost of $0.02 per kilowatt-hour over a five-year term with two successive three-year renewal options. The Nautilus Cryptomine Facility commenced mining in February 2023 and as of March 30, 2023, TeraWulf has approximately 10,000 miners energized, representing approximately 1.0 EH/S of self-mining capacity. TeraWulf expects to reach its full 50 MW capacity at the facility, representing approximately 16,000 miners, in the second quarter of 2023. TeraWulf has the option to add an additional 50 MW of bitcoin mining capacity, for a total of 100 MW, at the Nautilus Cryptomine Facility.

Subject to strategic development plans and the prevailing market prices and mining economics of bitcoin, TeraWulf’s management and board of directors may decide to exchange bitcoin for fiat currency through over-the-counter providers or exchanges to fund operations and future growth. While TeraWulf has relationships with over-the-counter providers and digital asset exchanges, TeraWulf does not have a contractual obligation as of the date of this Annual Report to convert bitcoin into fiat currency using any one provider and/or exchange. Currency exchange fees vary by provider and amount of digital asset being converted. TeraWulf anticipates conversion fees to the third-party providers to be in the range of approximately 0% to 0.25%. As of the date of this Annual Report, TeraWulf does not plan to convert bitcoin into other digital assets.

Agreements Relating to TeraWulf’s Business and Operations

Equipment Supply Agreements

Bitmain Agreements

On June 15, 2021, Nautilus executed (i) the non-fixed price sales and purchase agreement (the “First Quarter 2022 Bitmain Agreement”) with Bitmain to purchase 15,000 S19j Pro miners , with originally scheduled monthly deliveries of 5,000 miners each

4

between January 2022 and March 2022 and (ii) the non-fixed price sales and purchase agreement (the “Second Quarter 2022 Bitmain Agreement” and, together with the First Quarter 2022 Bitmain Agreement, the “2022 Bitmain Agreements”) with Bitmain to purchase 15,000 S19j Pro miners, with originally scheduled monthly deliveries of 5,000 miners each between April 2022 and June 2022. In 2022, the Company paid Bitmain $22.8 million and was reimbursed by Talen for 50% of that amount. In 2021, the Company paid Bitmain approximately $124.6 million under the 2022 Bitmain Agreements. On a net basis, the Company funded approximately $76.9 million as Talen reimbursed the Company in 2021 approximately $47.7 million in accordance with the Nautilus Cryptomine Joint Venture Agreement. As of December 31, 2022, the First Quarter 2022 Bitmain Agreement had concluded with all parties performing thereunder. In September 2022, the Second Quarter 2022 Bitmain Agreement was cancelled whereby each Nautilus member received a $31.2 million credit with Bitmain to use at the respective Nautilus member’s discretion (the “Bitmain Credit”). Additionally, approximately 5,000 of the miners ordered under the First Quarter 2022 Bitmain Agreement were delivered to the Lake Mariner Facility to be deployed there, pursuant to that certain exchange agreement by and between TeraWulf (Thales) LLC (“TeraWulf (Thales)”), Cumulus Coin LLC (“Cumulus Coin”) and Nautilus, entered into on March 14, 2022 and the August 27, 2022 amended and restated Talen Joint Venture Agreement. See “—Talen Joint Venture—Talen Joint Venture Agreement.”

On December 7, 2021, the Company entered into a Non-fixed Price Sales and Purchase Agreement with Bitmain for the purchase of 3,000 S19XP miners, with originally scheduled monthly deliveries of 500 miners each between July 2022 and December 2022 (the “Second Bitmain Purchase Agreement”) for a total purchase price of $32.6 million. For a batch of miners comprising a monthly shipment, if timely payments were made on installments then due, the Company holds an option to partially or wholly cancel such batch of miners and the remaining balance on such batch shall be refunded no later than two years after the cancellation. The Company is responsible for all transportation-related logistics costs for the delivery of miners. Pursuant to the Second Bitmain Purchase Agreement, the Company paid $2.0 million during the nine months ended September 30, 2022 and paid an initial deposit of approximately $11.4 in 2021. In September 2022, the Company cancelled the September and October 2022 batches, and the payments previously made for these monthly batches were applied to other payment obligations under the contract. Additionally, certain amounts from the Bitmain Credit were applied to the Second Bitmain Purchase Agreement. Subsequently, the Company cancelled the November and December 2022 batches and payments previously made and credits previously applied to this agreement became available as account credits for use in new purchasing arrangements with Bitmain. The Company considers the Second Bitmain Purchase Agreement to be concluded.

On December 15, 2021, the Company entered into a Non-fixed Price Sales and Purchase Agreement with Bitmain for the purchase of 15,000 S19XP miners, with originally scheduled monthly deliveries of 2,500 miners each between July 2022 and December 2022 (the “Third Bitmain Purchase Agreement”) for a total purchase price of $169.1 million. For a batch of miners comprising a monthly shipment, if timely payments were made on installments then due, the Company holds an option to partially or wholly cancel such batch of miners, and the remaining balance on such batch shall be refunded no later than two years after the cancellation. The Company is responsible for all transportation-related logistics costs for the delivery of miners. Pursuant to the Third Bitmain Purchase Agreement, the Company paid $10.2 million during the nine months ended September 30, 2022 and paid an initial deposit of approximately $59.2 million in 2021. In September 2022, the Company cancelled the September and October 2022 batches and payments previously made for these monthly batches were applied to other payment obligations under the contract. Additionally, certain amounts from the Bitmain Credit have been applied to the Third Bitmain Purchase Agreement. Subsequently, the Company cancelled the November and December 2022 batches and payments previously made and credits previously applied to this agreement became available as account credits for use in new purchasing arrangements with Bitmain. The Company considers the Third Bitmain Purchase Agreement to be concluded.

On September 28, 2022, the Company entered into two Future Sales and Purchase Agreements with Bitmain for the aggregate purchase of 3,400 S19XP miners and 2,700 S19 Pro miners, with originally scheduled monthly deliveries between October 2022 and January 2023 (the “September 2022 Bitmain Purchase Agreements”) for a total purchase price of $23.7 million. The purchase price will be satisfied through application of the balance of the Bitmain Credit.

On November 4, 2022, the Company entered into two Future Sales and Purchase Agreements with Bitmain for the aggregate purchase of 3,600 S19XP miners and 2,750 S19 Pro miners, with originally scheduled monthly deliveries between November 2022 and February 2023 (the “November 2022 Bitmain Purchase Agreements”) for a total purchase price of $24.9 million. The purchase price will be satisfied through application of the available account credits.

On December 5, 2022, the Company entered into a Future Sales and Purchase Agreement with Bitmain for the aggregate purchase of 14,000 S19 Pro miners, with originally scheduled monthly deliveries commencing December 2022 (the “December 2022 Bitmain Purchase Agreement”) for a total purchase price of $22.4 million. The purchase price will be satisfied through application of the available account credits.

5

Minerva Agreement

On March 19, 2021, TeraWulf executed an agreement for the purchase of bitcoin miners from Minerva Semiconductor Corp. (“Minerva”) for a total of 30,000 MV7 miners, with originally scheduled monthly deliveries of miners each between November 2021 and January 2022, for an aggregate price of $118.5 million (the “Minerva Purchase Agreement”). Pursuant to the Minerva Purchase Agreement, the Company paid an initial deposit of $23.7 million. Concurrently with the execution of the Nautilus Cryptomine Joint Venture agreement, TeraWulf assigned the Minerva Purchase Agreement to Nautilus During the period February 8, 2021 (date of inception) to December 31, 2021, the Company paid Minerva $16.8 million and was reimbursed by Talen for 50% of that amount and also reimbursed by Talen an additional amount of $11.9 million related to 50% of the initial deposit paid. The balance of payments under the Minerva Purchase Agreement were originally scheduled to be paid as follows: (i) 30% of the total price six months before the shipping date of each batch of bitcoin miners; (ii) 30% of the total price three months before the shipping date of each batch of bitcoin miners; and (iii) the remaining 20% of the total price one month before the shipping date of each batch of bitcoin miners. Production delays at Minerva’s factory have impacted the initial pricing and delivery schedule. Accordingly, Nautilus and Minerva have deemed all payments made to date to apply to the initial 9,000 miners to be shipped. As of March 30, 2023, Nautilus had not amended the Minerva Purchase Agreement.

Administrative and Infrastructure Services Agreement

On April 27, 2021, Beowulf E&D, a company owned and controlled by TeraWulf’s CEO, and TeraWulf entered into the administrative and infrastructure services agreement, pursuant to which Beowulf E&D agreed to provide, or to cause its affiliates to provide, to TeraWulf certain services necessary to buildout and operate certain bitcoin mining facilities anticipated to be developed by TeraWulf (the “Facilities”) and support TeraWulf’s ongoing business, including, among others, services related to construction, technical and engineering, operations and maintenance, procurement, information technology, regulatory, health and safety, treasury, finance and accounting, human resources, legal, corporate compliance, risk management, ESG, tax compliance, external affairs, corporate communications, public affairs and corporate planning and development. In addition, the administrative and infrastructure services agreement allows for Beowulf E&D to take actions in the name of TeraWulf, subject to certain limitations as set forth in the agreement. The administrative and infrastructure services agreement has an initial term of five years and automatically renews for successive three-year terms, unless earlier terminated.

Pursuant to the administrative and infrastructure services agreement, TeraWulf is required to (i) make available its professional, supervisory and managerial personnel employed by TeraWulf or its affiliates to coordinate with Beowulf E&D as reasonably required and (ii) provide Beowulf E&D access to the Facilities and any appurtenances thereto, together with the necessary rights of ingress and egress thereto. In addition, pursuant to the administrative and infrastructure services agreement, TeraWulf is responsible for obtaining, maintaining and renewing all permits necessary for TeraWulf to do business in the jurisdictions in which the Facilities are located and to own, operate and maintain the Facilities.

Pursuant to the administrative and infrastructure services agreement, Beowulf E&D may not provide infrastructure, construction, operations and maintenance or administrative services to any other persons in the bitcoin mining industry during the initial five-year term, other than those services provided by Beowulf E&D at the time of the execution of the administrative and infrastructure services agreement.

Pursuant to the administrative and infrastructure services agreement, TeraWulf appointed Beowulf E&D as agent with such authority as may be necessary for Beowulf E&D to perform the services pursuant to the administrative and infrastructure services agreement, including, among others, the authority to take actions and execute documents in the name, and as agent on behalf, of TeraWulf, subject, in all instances, to the limitations on Beowulf E&D’s authority set forth in the administrative and infrastructure services agreement and the specific written instructions of TeraWulf from time to time.

TeraWulf agreed to pay Beowulf E&D an annual fee for the first year in the amount of $7.0 million payable in monthly installments, and an annual fee equal to the greater of $10.0 million or $0.0037 per kilowatt-hour of electric load utilized by the Facilities thereafter. TeraWulf will also provide Beowulf E&D reimbursement for certain reasonable and documented equipment, infrastructure and operating expenses incurred in the performance of Beowulf E&D’s obligations under the administrative and infrastructure services agreement, which reimbursement will be prepaid monthly by TeraWulf and reconciled monthly. Beowulf E&D may also request advances for emergencies as well as equipment, infrastructure and operating expenses that require expedited payment terms.

6

In addition, in connection with the listing of its common stock, TeraWulf agreed to issue awards with respect to shares of its common stock to certain designated employees of Beowulf E&D in accordance with TeraWulf’s then effective omnibus incentive plan. Once the Facilities have utilized 100MW of cryptocurrency mining load in the aggregate, and for every incremental 100 MW of cryptocurrency mining load deployed by the Facilities in the aggregate thereafter, TeraWulf agreed to issue additional awards of shares of TeraWulf common stock to certain designated employees of Beowulf E&D in accordance with TeraWulf’s then effective omnibus incentive plan.

On March 29, 2023, TeraWulf and Beowulf E&D entered into Amendment No. 1 to the administrative and infrastructure services agreement, pursuant to which TeraWulf agreed to pay Beowulf E&D, effective as of January 1, 2023, a reduced annual base fee equal to $8.46 million payable in monthly installments, until all obligations under the Company’s Loan, Guaranty and Security Agreement dated as of December 1, 2021, as amended and restated from time to time, are either indefeasibly repaid in full or refinanced.

Lake Mariner Facility Lease

On June 1, 2021, Lake Mariner entered into the lease agreement (the “Lake Mariner Facility Lease”) with Somerset Operating Company, LLC (“Somerset”), a company 99.9%-owned and controlled by TeraWulf’s CEO, pursuant to which Lake Mariner agreed to lease from Somerset approximately 79 acres in the Town of Somerset, Niagara County, New York for an initial term of five years with an option to extend the term for additional five years on the same terms as the initial term with at least six months prior written notice from Lake Mariner to Somerset. On July 1, 2022, the Lake Mariner Facility Lease was amended (the “Lake Mariner Facility Lease Amendment”) to increase the initial term to eight years and to amend certain other non-financial sections to adjust environmental obligations, events of default and indemnification, site access rights and leasehold mortgage rights. Pursuant to the Lake Mariner Facility Lease Amendment, Lake Mariner, as tenant, irrevocably granted to the agent on behalf of the Company’s lenders under its Loan, Guaranty and Security Agreement, in its capacity as a leasehold mortgagee, a right of first refusal with respect to any assignment by Lake Mariner of the Lake Mariner Facility Lease.

The Lake Mariner Facility Lease contemplates that Lake Mariner will construct, or cause to be constructed, one or more buildings and/or ancillary structures (collectively, the “Building”) to be used as a cryptocurrency mining facility with ancillary services reasonably related thereto. Upon expiration of the Lake Mariner Facility Lease, the Building, together with all other buildings and improvements located thereon, will revert to Somerset. Lake Mariner has the right, at its own cost and expense, to erect and install on the premises additional buildings, driveways, improvements, signs and personal property or to make alterations to or replace existing buildings or improvements thereto as it deems necessary. Lake Mariner is required, at its sole cost and expense, to obtain all permits and approvals necessary to construct and operate a cryptocurrency mining facility.

Lake Mariner agreed to pay rent to Somerset in the annual amount of $150,000, payable in advance in equal monthly installments commencing on the first day of the calendar month immediately following the earlier to occur of (i) commencement of the initial construction of the Building or any ancillary structures to be used as a cryptocurrency mining facility with ancillary services reasonably related thereto or (ii) the 180th day after date of execution of the Lake Mariner Facility Lease. Lake Mariner is also responsible for paying any and all costs and expenses related to the premises and the leasehold estate, including, among others, real estate taxes, insurance, maintenance, repair, utilities and all other obligations whether similar or dissimilar to the foregoing.

Award for the Sale of High-Load Factor Power

On March 31, 2020, NYPA awarded TeraWulf a 90 MW allocation of high-load factor power for the Lake Mariner Facility for the sale of high-load factor power and NYPA’s Service Tariff No. HLF-1 (the “PPA”). On February 14, 2022, the Company executed the PPA with a term of ten years from the date of commencement of NYPA’s power delivery. Under the PPA, Lake Mariner is responsible for paying NYPA for unforced capacity, any fees associated with transmission and delivery of power and energy and a monthly clean energy implementation charge.

Wendel Agreement

On September 17, 2021, Wendel Construction, Inc., as subcontractor, Beowulf E&D, as contractor and TeraWulf, as owner, entered into the Project Build Subcontract Agreement to substantially build the Lake Mariner Facility (as amended by that certain 2nd Amendment to Project Build Subcontract Agreement, the “Wendel Agreement”). The Wendel Agreement provided that TeraWulf pay Wendel for their performance of the work, with a Control Estimate (as defined therein) of approximately $47.1 million. Pursuant to the terms of the Wendel Agreement, TeraWulf was responsible for maintaining an escrow account balance that, when added to the

7

unexpended Advance Payment (as defined therein), was equal to $3.0 million or 100% of the remaining project costs, whichever was less, by the 15th day of each month until the earlier of (i) the date on which the project is completed and (ii) the date on which the agreement terminates. Progress payments on the Wendel Agreement are made monthly through the escrow account.

On March 9, 2022, the Wendel Agreement was amended to expand the scope of work to include the design and construction of an additional building, building #3, to house approximately 15,000 additional miners with an electrical capacity of approximately 50 megawatts. Wendel retained five sub-subcontractors to perform various work under the Wendel Agreement.

On March 6, 2023, TeraWulf, Beowulf E&D and Wendel entered into a mutual termination agreement pursuant to which the Wendel Agreement was terminated in all respects, effective as of December 13, 2022. Under the terms of the mutual termination agreement, Wendel agreed to pay approx. $1.86 million to its sub- subcontractors, assigned five sub-subcontracts to Beowulf E&D and Beowulf assumed the remaining financial obligations thereunder in an amount of approx. $435,000. As of March 6, 2023, construction of building #1 of the Lake Mariner Facility was complete, construction of building #2 was partially complete and the design of building #3 was complete.

Custody and Sales of Bitcoin

NYDIG Custodial Agreement

On March 10, 2022, we entered into a Digital Asset Custodial Agreement with NYDIG (the “NYDIG Custodial Agreement") pursuant to which NYDIG holds our bitcoin in cold storage as custodian in a digital asset account in the Company’s name (the “Digital Asset Account”), In exchange for its custodial services, NYDIG charges an annual fee equal to a percentage of our custodied bitcoin, based on its daily average value in U.S. Dollars. Our bitcoin in the Digital Asset Account does not constitute “deposits” within the meaning of U.S. federal or state banking law. Balances of digital assets in the Company’s Digital Asset Account are not subject to Federal Deposit Insurance Corporation (“FDIC”) or Securities Investor Protection Corporation (“SIPC”) protections.

NYDIG holds the Company’s bitcoin in trust for our benefit, and NYDIG has no right, interest or title in our custodied bitcoin. Beneficial and legal ownership of all our bitcoin remains freely transferable without the payment of money or value and NYDIG has no ownership in the Company’s custodied bitcoin. The Company’s bitcoin does not constitute an asset on NYDIG’s balance sheet and will at all times be identifiable in NYDIG’s database as being stored in the Company’s Digital Asset Account for our benefit. The Company’s bitcoin is held in the Digital Asset Account at all times and is not commingled with other digital assets held by NYDIG, whether for its own account or the account of others, except temporarily (typically for no longer than 12 hours, but in no case longer than 72 hours) as an operational matter, if required, to effect a transfer into our out of our Digital Asset Account.

NYDIG is not permitted to transfer any of our custodied bitcoin except as expressly directed by the Company pursuant to a designated security procedure. NYDIG maintains policies, procedures and practices reasonably designed to comply with the New York Department of Financial Services’ Cybersecurity Regulation (23 NYCRR 500). Transfers of the Company’s bitcoin requires private keys stored on one or more servers, hard drives, or other media physically present at a location in the United States. No physical, operational and cryptographic system for the secure storage of private keys is perfectly secure, and loss or theft due to operational or other failure is always possible. NYDIG does not guarantee the value of the Company’s bitcoin. NYDIG does not control any decentralized peer-to-peer network used to transfer bitcoin (“Digital Asset Network”) and is not responsible for the services provided by those Digital Asset Networks. The software and cryptography that governs the protocols of Digital Asset Networks have short histories and could at any time be found ineffective or faulty, which could result in the complete loss of value or theft of our custodied bitcoin. NYDIG has established a business continuity plan that will support its ability to conduct business in the event of a significant business disruption, which is reviewed and updated annually.

To the extent NYDIG does not cause or contribute to a loss the Company suffers in connection with any bitcoin transaction initiated, NYDIG has no liability for that loss. In the event NYDIG fails to (1) execute a properly executable instruction of the Company and (2) give the Company notice of such failure, NYDIG will only be liable for our actual damages. In no event will either be liable for any indirect, incidental, special or consequential losses. Either party’s total aggregate liability arising out of or relating to the NYDIG Custodial Agreement is limited to the greater of (1) the fair market value of the amount of the Company’s custodied bitcoin at the time in which the events giving rise to the liability occurred and (2) the fair market value of the amount of our custodied bitcoin at the time that NYDIG notifies us in writing or we otherwise have actual knowledge of the events giving rise to the liability. The fair market value of each digital asset will be determined by NYDIG according to its valuation policy, which may differ from the way the Company values its digital asset holdings The NYDIG Custodial Agreement has a term of one ear and renews automatically for successive one-year periods, unless terminated by either party upon 30 days prior written notice.

8

NYDIG Execution Agreement

On September 16, 2022, we entered into a Digital Asset Execution Agreement (the “Execution Agreement”) with NYDIG Execution pursuant to which NYDIG Execution executes or arranges our bitcoin sales orders (“Orders”) as our agent. NYDIG Execution may execute the Company’s Orders against one of its customers or counterparties, on a digital asset exchange, or against NYDIG Execution or other NYDIG affiliate. We deliver our Orders to NYDIG Execution via a designated security procedure, and each Order is affirmatively accepted by NYDIG Execution. While the Company’s bitcoin may temporarily be processed through a NYDIG Execution customer account, our bitcoin is not commingled with the assets of NYDIG Execution. NYDIG Execution deposits any cash from the sale of the Company’s bitcoin directly into the Company’s bank account at a U.S. depositary institution, less any applicable commissions, fees or costs. NYDIG Execution does not guarantee the value of our bitcoin, does not control any Digital Asset Network and is not responsible for any delay or failure to complete any Order caused by a Digital Asset Network. If NYDIG Execution fails to (1) execute a properly executable Order and (2) give the Company notice of such failure, NYDIG Execution will only be liable for our actual damages. In no event will NYDIG Execution be liable for any consequential, indirect, special or punitive damages. NYDIG Execution or the Company can terminate the Execution Agreement upon thirty days prior written notice.

Mining Pool Services

Foundry Digital Services Agreement

We entered into a Service Agreement (“Service Agreement”) with Foundry Digital LLC (“Foundry”) by accessing and using the Pool (defined below) pursuant to which Foundry provides us with a digital currency mining pool (“Pool”) and other services/products that may be added based on the Pool site (“Service”). The Pool and Service provided by Foundry does not include wallet or custodial services. We have authorized Foundry to be fully responsible for the disposal and distribution of the profits from the Service. Foundry may modify or interrupt the Service at any time without informing us and without liability to us or any third party not directly related. Foundry has the right to modify the Service Agreement at any time. If we do not agree to the Service Agreement or any of its modifications, then we must cease to use the Pool and will not be allowed further access to the Pool and Service. We are using the Pool and Service at our own risk. In the event that our access and/or rights to the Pool and Service are discontinued, we are solely responsible for settling the remaining balances left in our account. Foundry must use commercially reasonable efforts to assist us with settling any remaining balances in our account. Foundry is not responsible or liable to us for any balances remaining in our account three months after our access and/or rights to the Pool and Service have been discontinued (regardless of whether the balances were left in our account intentionally). The Service Agreement remains in effect until our access and usage rights to the Pool and Service are terminated by either us or Foundry. We may terminate the Service Agreement at any time upon settlement of any pending transactions. Foundry may, at its sole discretion, limit, suspend or terminate our access to the Pool and Service if: (i) we become subject to bankruptcy/insolvency proceedings, (ii) we liquidate, dissolve, terminate or suspend our business, (iii) we breach the Service Agreement or (iv) we perform any act or omission that materially impacts our ability to adhere to the Service Agreement.

As described further in the section titled “Risk Factors” herein, even though we do not hold any cryptocurrency on others’ behalf and do not currently sell or intend to sell our cryptocurrency on exchanges, our business, financial condition and results of operations may still be adversely affected by recent industry-wide developments beyond our control, including the continued industry-wide fallout from the recent Chapter 11 bankruptcy filings of cryptocurrency exchange FTX Trading Ltd., et al. (“FTX”) (including its affiliated hedge fund Alameda Research LLC), crypto hedge fund Three Arrows Capital (“Three Arrows”) and crypto lenders Celsius Network LLC, et al. (“Celsius”), Voyager Digital Ltd., et al. (“Voyager”), BlockFi Inc., et al. (“BlockFi”) and Genesis Global Holdco, LLC, et al. (“Genesis”). Most recently, in January 2023, Genesis filed for Chapter 11 bankruptcy. Genesis is owned by Digital Currency Group Inc. (“DCG”), who also owns Foundry, our mining pool provider. At this time, there are no material risks to our business arising from our indirect exposure to Genesis. Although (i) our cryptocurrency mining business has no direct exposure to any of the cryptocurrency market participants that recently filed for Chapter 11 bankruptcy; (ii) we have no assets, material or otherwise, that may not be recovered due to these bankruptcies; (iii) we have no direct exposure to any other counterparties, customers, custodians or other crypto asset market participants known to have (x) experienced excessive redemptions or suspended redemptions or withdrawal of crypto assets, (y) the crypto assets of their customers unaccounted for, or (z) experienced material corporate compliance failures; and (iv) our activities in the commercial optimization of the power supply are unaffected by the recent crypto market events; our business, financial condition and results of operations may not be immune to unfavorable investor sentiment resulting from these recent developments in the broader cryptocurrency industry.

9

Talen Joint Venture

Talen Joint Venture Agreement

On May 13, 2021, TeraWulf (Thales) entered into a limited liability company agreement (the “Talen Joint Venture Agreement”) with Cumulus Coin, an affiliate of Talen, to develop, construct and operate up to 300 MW of zero-carbon bitcoin mining in Pennsylvania (the “Nautilus Cryptomine Facility”). Each member originally held a 50% interest in Nautilus. Pursuant to the terms of the Talen Joint Venture Agreement, TeraWulf would contribute $156.0 million both in cash and in-kind and Talen would contribute $156.0 million both in cash and in-kind to Nautilus by March 2022, unless otherwise determined in accordance with the Talen Joint Venture Agreement.

On August 27, 2022, the members entered into an amended and restated Joint Venture agreement (the “A&R Talen Joint Venture Agreement”) whereby, among other changes, the unit ownership will be determined by infrastructure contributions while distributions of mined bitcoin will be determined by each member’s respective hashrate contributions. Members are allowed to make contributions of miners up to the effective electrical capacity of their owned infrastructure percentage. Each member retains access to 50% of the electricity supply outlined in the Nautilus Cryptomine Facility Ground Lease. Additionally, the Company’s scheduled capital contributions were amended such that the Company would retain a 33% ownership interest in the Joint Venture if such capital contributions were funded. With the change in ownership percentage, governance rights were amended to provide for greater Talen board participation, among other changes. Subsequent to September 30, 2022, the Company targeted a 25% ownership interest in Nautilus and therefore made $7.3 million of the scheduled $17.1 million capital contributions. The Company is not obligated to fund the balance of the $17.1 million scheduled infrastructure-related capital contributions. Accordingly, the Company’s ownership interest in Nautilus as of March 30, 2023 is 25%. Further, Nautilus is governed by a board of managers comprised of one manager appointed by TeraWulf and four managers appointed by Talen.

Pursuant to the terms of the Talen Joint Venture Agreement, the Nautilus Cryptomine Facility will initially require 100 MW of electric capacity, and Nautilus may elect to expand the energy requirement to up to 300 MW prior to May 13, 2024. Upon such election, Nautilus will call additional capital for expansion and enter into an additional energy supply agreement with Talen for the additional capacity, subject to any regulatory approvals and third-party consents. Unless terminated earlier in accordance with the terms of the Talen Joint Venture Agreement, until May 13, 2023, Talen will not provide any electrical capacity at the site of the Nautilus Cryptomine Facility to any third party that is principally engaged in, or that has publicly disclosed its intention to become engaged in, or otherwise intends to use, electrical capacity for bitcoin mining or bitcoin transaction verification at the site.

Nautilus and TeraWulf (Thales) entered into an exchange agreement on March 14, 2022, pursuant to which Nautilus sold to TeraWulf (Thales) 2,500 Bitmain S19j Pro bitcoin mining machines (the “Nautilus Miners”) in exchange for an equivalent number of BTC mining machines which are new and either identical to or which, in the reasonable good faith opinion of Cumulus Coin, in the aggregate, function and perform in a manner no less effective in respect of mining BTC than the Nautilus Miners (the “Exchange Miners”). The A&R Talen Joint Venture Agreement removed the Company’s obligation to deliver the Exchange Miners to Nautilus.

In accordance with the terms and provisions of the Talen Joint Venture Agreement, TeraWulf and Talen entered into (i) the Nautilus Cryptomine Facility Ground Lease, (ii) the Beowulf E&D Facility Operations Agreement relating to the operation of the Nautilus Cryptomine Facility and (iii) the Talen Corporate Services Agreement relating to the provision of corporate and administrative services to Nautilus. In addition, in accordance with the terms and provisions of the Talen Joint Venture Agreement, the Minerva Agreement was assigned from TeraWulf to Nautilus.

On March 23, 2023, TeraWulf (Thales) entered into a second amended and restated limited liability company agreement (the “Second A&R Talen Joint Venture Agreement”) with Cumulus Coin. Under the Second A&R Talen Joint Venture Agreement, TeraWulf (Thales) will hold a 25% equity interest in Nautilus and Cumulus Coin will hold a 75% equity interest in Nautilus, each subject to adjustment based on relative capital contributions. Bitcoin distributions will be made every two weeks in accordance with each Member’s respective hash rate contributions after deducting each Member’s share of power and operational costs and cash reserves, as established by the board of managers, to fund, among other things, one month of estimated power costs and two months of budgeted expenditures.

Under the Second A&R Talen Joint Venture Agreement, each member will be entitled to make contributions to Nautilus of certain miners up to a maximum determined in accordance with each member’s ownership percentage, by delivering or causing to be delivered and installed or deemed installed on behalf of Nautilus at the Nautilus Cryptomine facility or at Nautilus’ storage facility, such miners. Pursuant to the Second A&R Talen Joint Venture Agreement, certain MinerVa miners that TeraWulf (Thales)

10

contributed to Nautilus will be removed and provided to TeraWulf (Thales), which TeraWulf (Thales) has the right to replace in its discretion. Likewise, Cumulus Coin may elect to remove certain MinerVa miners that Cumulus Coin contributed to Nautilus, which Cumulus Coin has the right to replace in its discretion.

Nautilus will be governed by a board of managers comprised of one manager appointed by TeraWulf (Thales) and four managers appointed by Cumulus Coin. Under the Second A&R Talen Joint Venture Agreement, the board of managers generally acts upon a majority vote at a duly called meeting at which the manager appointed by TeraWulf (Thales) is present, except that, for certain specified matters (“Special Consent Matters”), the board of managers acts upon a unanimous vote, subject to deadlock procedures. Any Member owning less than 20% of Nautilus has no right to vote on Special Consent Matters. Generally, neither TeraWulf (Thales) nor Cumulus Coin may directly transfer any of its interests in Nautilus to any third parties without the majority consent of the board of managers, except that TeraWulf (Thales) is entitled to transfer its interests in Nautilus if certain conditions are met.

Pursuant to the terms of the Second A&R Talen Joint Venture Agreement, the Nautilus Cryptomine facility will initially require 200 MW of electric capacity, and the Cumulus Coin may elect to expand the energy requirement by up to 100 MW, funded solely by the Cumulus Coin, prior to May 13, 2024, for a total capacity of 300 MW. Upon such election, Nautilus will call additional capital for expansion and enter into an additional energy supply agreement with Cumulus Coin or its affiliate for the additional capacity, subject to any regulatory approvals and third-party consents.

On August 26, 2022, Nautilus and Beowulf E&D entered into an amended and restated facility operations agreement with an early termination right for Nautilus, pursuant to which Beowulf E&D provides, or arranges for the provision to Nautilus of, certain infrastructure, construction, operations and maintenance and administrative services necessary to build out and operate the Nautilus Cryptomine facility and support Nautilus’s ongoing business at the Nautilus Cryptomine facility. Nautilus terminated the amended and restated facility operations agreement effective December 26, 2022. On December 26, 2022, Nautilus and Talen Energy Supply LLC entered into a replacement facility operations agreement pursuant to which Talen Energy Supply LLC provides, or arranges for the provision to Nautilus of, certain infrastructure, construction, operations and maintenance and administrative services necessary to build out and operate the Nautilus Cryptomine facility and support Nautilus’s ongoing business at the Nautilus Cryptomine facility. Also on December 26, 2022, Beowulf E&D and Nautilus entered into a transition services agreement to facilitate the prompt transition of the services provided by Beowulf E&D to Nautilus under the amended and restated facility operations agreement to Talen Energy Supply LLC. Pursuant to the transition services agreement, Beowulf E&D shall provide such transition services to Nautilus until June 30, 2023 in exchange for payment by Nautilus of $339,200 and reimbursement of out of pocket expenses.

Nautilus Cryptomine Facility Ground Lease

Susquehanna Data LLC, a Delaware limited liability company, as assigned by Talen Nuclear Development LLC, a Delaware limited liability company, as lessor (in such capacity, the “Lessor”), and Nautilus, as lessee (in such capacity, the “Lessee”), entered into the ground lease, dated as of May 13, 2021 (the “Nautilus Cryptomine Facility Ground Lease”), for certain premises located on the campus of the Susquehanna Station. The purpose of the Nautilus Cryptomine Facility Ground Lease is to provide the Lessee with an interest in the land for the design, construction and operation of a bitcoin mining facility site, consisting of one or more buildings and related facilities necessary for its operation.

The term of the Nautilus Cryptomine Facility Ground Lease runs for a period of five years, beginning on the date that the Lessee begins mining operations, but no later than June 15, 2022 (the “Commencement Date”). At the end of the initial term, the Lessee will have two options to renew the Nautilus Cryptomine Facility Ground Lease for three years each, and, pursuant to an amendment dated December 28, 2022 to the Nautilus Cryptomine Facility Ground Lease (the “Nautilus Cryptomine Facility Ground Lease Amendment”), an option to extend the term by an interim period of up to six and one half months after the first three year renewal term. Prior to the Commencement Date, the Lessee’s initial base rent is $22,012 per month, which begins on the first day of the first calendar month following the date on which electric power is first made available to the premises sufficient to satisfy the Lessee’s initial energy requirement (“COD”). After the Commencement Date, base rent increases to $131,906 per month for the duration of the term of the Nautilus Cryptomine Facility Ground Lease. In the Nautilus Cryptomine Facility Ground Lease Amendment, the parties confirmed June 15, 2022 as the Commencement Date and July 1, 2022 as the date on which the base rent will increase. The Lessee notified the Lessor that COD occurred on February 14, 2023. The Lessee is responsible for paying additional rent for property taxes, as well as the Lessee’s proportionate share of the Lessor’s operating expenses incurred in the ownership, operation and maintenance of any shared facilities and common areas on the campus. The Lessee is responsible for reimbursing the Lessor for all costs to construct a dedicated substation serving the Nautilus Cryptomine Facility, as such costs are amortized with an interest of 8% per annum over 11 years. The Lessee is also responsible for all costs for the repair and maintenance of the substation.

11

Another component of compensation under the Nautilus Cryptomine Facility Ground Lease is a provision of power by the Lessor to the Lessee (the “Nautilus Cryptomine Facility Power Purchase Agreement”). Pursuant to the terms of the Nautilus Cryptomine Facility Power Purchase Agreement, electricity will be furnished by the Lessor to the Lessee on a “sub-metering” basis. So long as electric current is supplied by sub-metering, the Lessee will pay to the Lessor a delivered energy charge each month of the term of the Nautilus Cryptomine Facility Power Purchase Agreement. If the Lessee’s capacity factor is below 95% during any such month beginning March 1, 2023, the Lessee is required to pay an additional capacity charge to the Lessor of $4.82 per MW-hour of any capacity shortage.

Beowulf E&D Facility Operations Agreement

On May 13, 2021, Nautilus and Beowulf E&D entered into the facility operations agreement (the “Beowulf E&D Facility Operations Agreement”), pursuant to which Beowulf E&D agreed to provide, or arrange for the provision to Nautilus of, certain infrastructure, construction, operations and maintenance and administrative services necessary to build out and operate the Nautilus Cryptomine Facility and support Nautilus’s ongoing business at the Nautilus Cryptomine Facility. Nautilus agreed to pay Beowulf E&D an annual fee in the amount of $750,000 payable annually in advance and reimburse Beowulf E&D for all out-of-pocket fees, expenses and capital costs paid by Beowulf E&D or its affiliates.

On August 27, 2022, the Nautilus and Beowulf E&D entered into an amended and restated Beowulf E&D Facility Operations Agreement (the “A&R Beowulf E&D Facility Operations Agreement”) in connection with the A&R Talen Joint Venture Agreement to provide that the term of the A&R Beowulf E&D Facility Operations Agreement remain in effect until the earliest of (i) August 27, 2025, (ii) its termination by mutual consent of Nautilus and Beowulf E&D, (iii) the sale by TeraWulf and its affiliates of their interests in Nautilus, (iv) the consummation of an initial public offering of Nautilus, (v) termination by either party in the event of a default by the other party or (vi) termination by Nautilus for convenience upon at least ninety days prior written notice. Pursuant to the terms of the A&R Beowulf E&D Facility Operations Agreement, if Nautilus terminates the agreement for convenience between July 1, 2022 and June 30, 2023, Nautilus shall pay Beowulf E&D a termination fee in the amount of $1,750,000, or after June 30, 2023, Nautilus shall pay Beowulf E&D a termination fee in the amount of in the amount of $750,000. Nautilus terminated the A&R Beowulf E&D Facility Operations Agreement for convenience effective December 26, 2022.

On December 26, 2022, Beowulf E&D and Nautilus entered into a Transition Services Agreement (the “Transition Services Agreement”) to facilitate the prompt transition of the services provided by Beowulf E&D to Nautilus under the A&R Beowulf E&D Facility Operations Agreement to Talen Energy Supply LLC, the successor provider of infrastructure, construction, operations and maintenance and administrative services to Nautilus. The Transition Services Agreement provides for Beowulf E&D to provide such transition services to Nautilus until June 30, 2023 in exchange for payment by Nautilus of $339,200 payable monthly in advance commencing on January 1, 2023 and reimbursement of out of pocket expenses.

Talen Corporate Services Agreement

On August 27, 2022 and effective as of May 13, 2021, Nautilus and Cumulus Digital, LLC (“Cumulus Digital”) entered into an amended and restated corporate services agreement (the “A&R Talen Corporate Services Agreement”), pursuant to which Cumulus Digital will provide certain corporate and administrative services to Nautilus, including all day-today corporate-level management and support services such as accounting and financial reporting, development planning, real estate, information technology, financial planning and analysis, banking, treasury, regulatory, legal, supply chain and secretarial and administrative functions. Nautilus agreed to pay Cumulus Digital an annual fee in the amount of $750,000 payable annually in advance and reimburse Cumulus Digital for all out-of-pocket fees, expenses and capital costs paid by Cumulus Digital or its affiliates.

The term of the A&R Talen Corporate Services Agreement will continue until the earliest of (i) August 27, 2025, (ii) its termination by mutual consent of Nautilus and Talen Energy Supply, (iii) the sale by Cumulus Coin and its affiliates of their interests in Nautilus, (iv) the consummation of an initial public offering of Nautilus, (v) the termination of the Talen Corporate Services Agreement by either party in the event of a default by the other party or (vi) termination by Nautilus for convenience upon at least ninety days prior written notice. Pursuant to the terms of the A&R Talen Corporate Services Agreement, if Nautilus terminates the agreement for convenience between July 1, 2022 and June 30, 2023, Nautilus shall pay Cumulus Digital a termination fee in the amount of $1,750,000, or after June 30, 2023, Nautilus shall pay Cumulus Digital a termination fee in the amount of in the amount of $750,000.

12

Loan, Guaranty and Security Agreement

On December 1, 2021, TeraCub entered into a Loan, Guaranty and Security Agreement with Wilmington Trust, National Association as administrative agent (the “LGSA”). The LGSA consists of a $123.5 million term loan facility (the “Term Loan”). On December 14, 2021, TeraWulf executed a joinder agreement whereby it effectively became the successor borrower to TeraCub and assumed all obligations under the LGSA. The Company is required to pay the outstanding principal balance of the Term Loan in quarterly installments, commencing in April 2023, equal to 12.5% of the original principal amount of the Term Loan. The maturity date of the Term Loan is December 1, 2024. The Term Loan bears an interest rate of 11.5% and an upfront fee of 1%, an amount of approximately $1.2 million. Upon the occurrence and during the continuance of an event of default, as defined, the applicable interest rate will be 13.5%. Interest payments are due quarterly in arrears. The Company has the option to prepay all or any portion of the Term Loan in increments of at least $5.0 million subject to certain prepayment fees, including: (1) if paid prior to the first anniversary of the LGSA, a make whole amount based on the present value of the unpaid interest that would have been paid on the prepaid principal amount over the first year of the Term Loan, (2) if paid subsequent to the first anniversary of the LGSA but prior to the second anniversary of the LGSA, an amount of 3% of the prepaid principal and (3) if paid subsequent to the second anniversary of the LGSA but prior to the maturity date of the LGSA, an amount of 2% of the prepaid principal. Certain events, as described in the LGSA, require mandatory prepayment. The Term Loan is guaranteed by TeraWulf Inc. and TeraCub and its subsidiaries, as defined, and is collateralized by substantially all of the properties, rights and assets of TeraWulf Inc. and TeraCub and its subsidiaries (except IKONICS), as defined. One Term Loan investor, NovaWulf Digital Master Fund, L.P., with a principal balance of $15.0 million, is a related party due to cumulative voting control by members of Company management and a member of the Company’s board of directors. In July 2022, NovaWulf Digital Master Fund, L.P. transferred a principal balance of $13.0 million of the Term Loan to NovaWulf Digital Private Fund LLC. In connection with the LGSA, the Company issued to the holders of the Term Loans 839,398 shares of Common Stock (the “Term Loan Equity”).

On July 1, 2022, the Company entered into an amendment to the LGSA. This amendment provides for an additional $50.0 million term loan facility (the “New Term Facility”). The New Term Facility has a maturity date of December 1, 2024, consistent with the existing term loans under the LGSA. The interest rate with respect to the New Term Facility is consistent with the existing term loans under the LGSA, but the interest rate under the amended LGSA may be increased, if applicable, to the cash interest rate on any junior capital raised plus 8.5%, if higher. No interest rate adjustment has been made under this provision. Pursuant to the New Term Facility, funds can be drawn in three tranches. The $15.0 million first tranche (the "First Amendment Term Loan") was drawn at closing in July 2022, and the subsequent tranches of up to $35 million (the “Delayed Draw Term Loan Commitment”) may be drawn at Company’s option prior to December 31, 2022, subject to certain conditions, including the raising of matching junior capital, as defined. The amortization with respect to the first tranche of the New Term Facility is consistent with existing term loans under the LGSA. The loans under the subsequent tranches of the New Term Facility are repayable in quarterly installments on (i) April 5, 2024 and July 8, 2024, equal to 12.50% of the original principal amount advanced under such tranches under the LGSA and (ii) October 7, 2024, equal to 37.5% of the original principal amount advanced under such tranches of the LGSA. The New Term Facility required the Company to extend the initial term of the Ground Lease from five years to eight years. The prepayment provisions remain unchanged for the Term Loan. If the New Term Facility is repaid within 121 days of July 1, 2022, then a 3% prepayment penalty is due. A prepayment thereafter results in no prepayment penalty.

In connection with the New Term Facility, the Company paid an upfront fee of $125,000 and issued warrants to the lenders under the New Term Facility to purchase 5,787,732 shares of Common Stock at $0.01 per share, an aggregate number of shares of the Company’s Common Stock equal to 5.0% (comprised of 2% related to the Delayed Draw Term Loan Commitment and 3% related to the First Amendment Term Loan) of the then fully diluted equity of the Company (the “Lender Warrants”). If the Company draws subsequent tranches, it is required to issue warrants to the lenders to purchase shares of the Company’s Common Stock equal to dilution of 3.75% upon the issuance of a second tranche in the amount of $15.0 million and 4.25% upon issuance of a third tranche in the amount of $20.0 million, in each case as a percentage of the then fully diluted equity of the Company, respectively. A certain portion of the Lender Warrants were subject to cancellation, upon the occurrence of certain conditions, but based on the passage of time no cancellation provisions remain effective. The Lender Warrants were subject to certain vesting restrictions, which expired on September 30, 2022 or October 30, 2022.

On August 26, 2022, TeraWulf Inc. (the “Company”) entered into a second amendment (the “Second Amendment”) to the LGSA. The LGSA, as amended, required the Company to maintain or meet certain affirmative, negative, financial and reporting covenants. The affirmative covenants include, among other things, a requirement for the Company to maintain insurance coverage, maintain mining equipment and comply in all material respects with the Company’s Nautilus joint venture agreement. The negative covenants restrict or limit the Company’s ability to, among other things, incur debt, create liens, divest or acquire assets, make restricted payments and permit the Company’s interest in the Nautilus joint venture to be reduced below 25%.

13

On October 7, 2022, the Company entered into a third amendment (the “Third Amendment”) to the LGSA, which divided the initial funding of up to $15,000,000 of the Delayed Draw Term Loan Commitment into two tranches of up to $7,500,000 each. The first tranche of $7,500,000 was borrowed upon the effectiveness of the Third Amendment on October 7, 2022. On the same date, the Company also entered into an amendment and restatement of that certain warrant agreement with respect to the Lender Warrants, which provided for their immediate exercisability.